To achieve a truly sustainable economy, we have to have a solution to the question “Where are we going to put all that carbon?” As it happens, geologic storage of carbon dioxide by injecting CO2 into old oil wells as a way to squeeze out those last drips of oil, commonly referred to as “Enhanced Oil Recovery,” has been an ongoing practice for over 40 years. This unintentional side-effect on its own, however, is nowhere near sufficient to address the levels of carbon in the atmosphere. With heightened concern and urgency around the climate crisis, companies have been committing resources to sequester more and more carbon, not only to meet ambitious emission reductions goals set by policy-makers and industry groups, but also to capture valuable tax credits and grants, including in the U.S. from newly passed legislation like the bipartisan Infrastructure Act of 2021 and the Inflation Reduction Act of 2022 (IRA). So, the question still stands, where are we putting all the carbon?

Energy demand will outstrip supply, but companies are seeking to decarbonize the energy supply

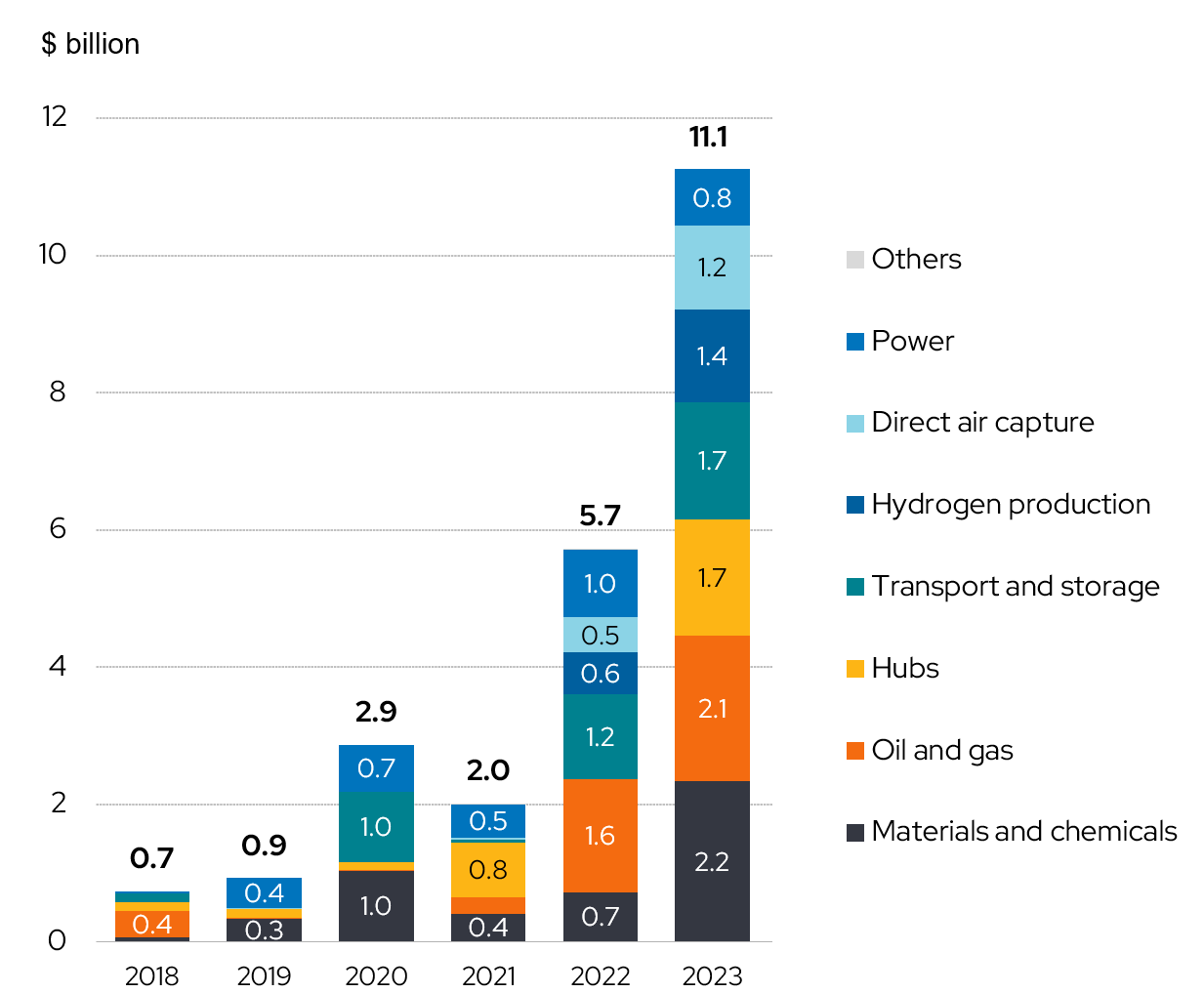

Energy demand is set to grow ~1.5% per year per capita, supplied by growth of new oil and gas projects, new solar and wind installations and a reduction in coal fueled energy.1 At our current rate of energy production across all sources, we are falling behind the energy curve, which will ultimately result in high energy prices.2 Simultaneously, with the growth of fossil fuel energy resources produced and the consensus view that global emissions need to come down significantly, companies have deployed over $20 billion into CCS over the past 5 years according to Bloomberg New Energy Finance.3

Sources: CCUS Market Outlook 1H 2024: Trough of Disillusionment. Bloomberg New Energy Finance (BNEF), June 3, 2024.

Got AI?

In data center power demand growth alone, Goldman Sachs estimates an additional 47,000 MW of incremental capacity will be needed through 2030, equating to over $560 billion over the next four years, which is a 36% increase over the previous four years.

Source: Green Capex: Reliability, Efficiency, Equivalency: Themes to resonate amid uncertainty. Goldman Sachs Investment Research (GIR), June 26, 2024.

Which technologies are we talking about?

We capture CO2 from fossil or biomass-fueled power stations, industrial facilities, and more experimentally, directly from the air. We then transport compressed CO2 by ship or pipeline from the point of capture to the point of usage, and in many situations, permanently store CO2 in underground geologic formations on-shore and offshore (IES, CCS Handbook, 2021).

The capturing of CO2 can be done pre-fuel combustion, post fuel combustion or through a process known as Oxy-Fuel combustion. In any case, the stream of gas is mixed with one of many different Amine Solvents in a heat exchanger and then CO2 is extracted from the solvent. The readiness level of these several of these technologies is a 9 out of 94, meaning they are ready for full commercial deployment. The costs of capturing carbon from power plants varies by technology, but the overwhelming largest cost is the capital expenditures companies are laying out which can run from $28-57 per metric ton of CO2. The largest market is the U.S. in terms of capacity and of million metrics tons stored per year.5

An Example: Methyl Diethanolamine (MEA) Scrubbing Process

(Source: US DOE, Carbon Dioxide Handbook, 2015)

Storing CO2 in underground formations has been demonstrated by structural trapping under an impermeable seal, dissolution and mineral trapping by saturating the CO2 in naturally occurring in brines, as well as precipitation of CO2 into rock calcium in the form of Calcium Carbonate (CaCO3).

According to the Global CCS Institute, in 2023, the capture capacity of CCS projects in development, in construction, or operating has increased 48% year-over-year, with almost a doubling of the number of facilities.

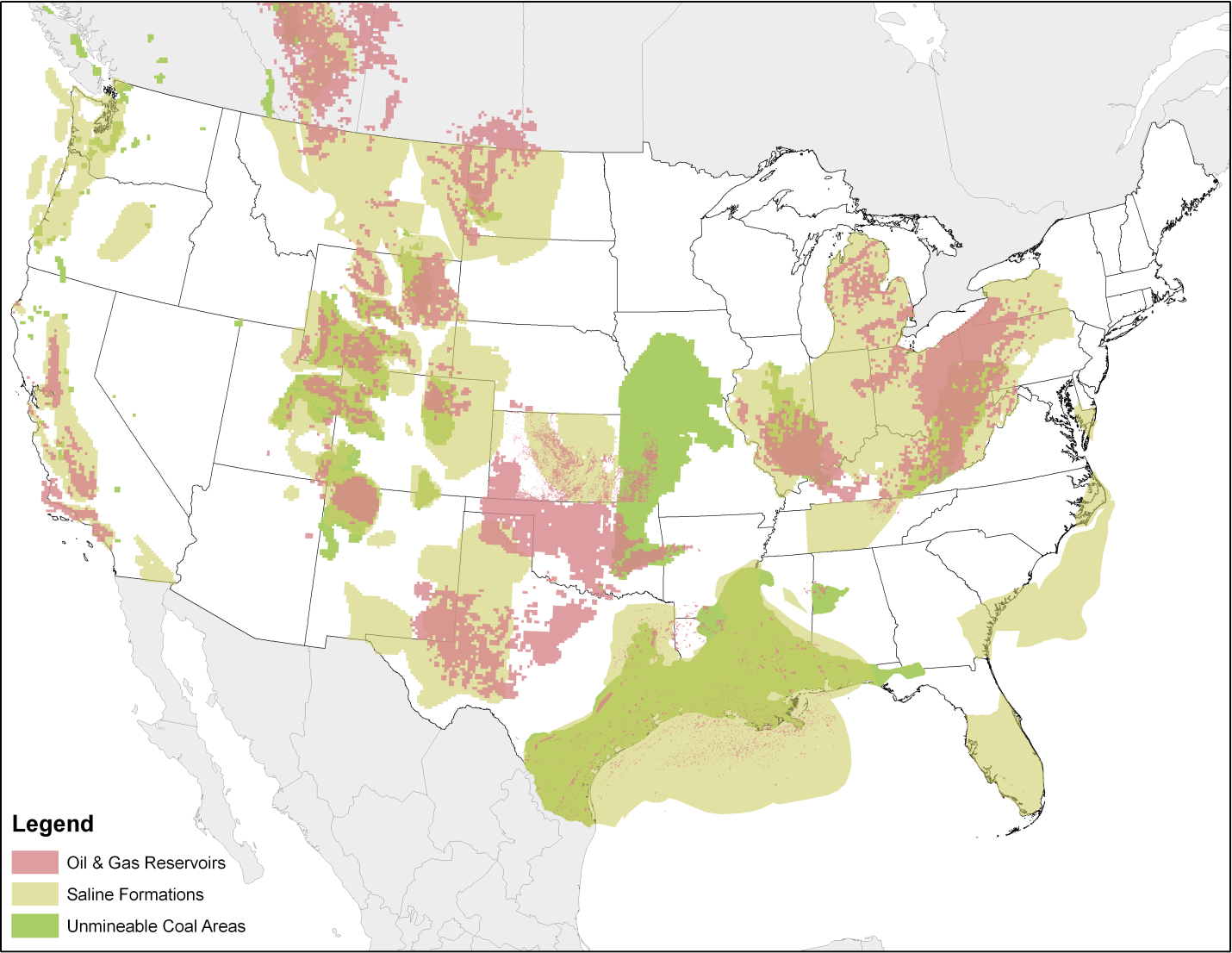

Transporting the CO2 by pipeline will need to expand rapidly but is not without hiccups in the form well permitting. A well capable of storing CO2, known as a Class VI well, requires permitting in the US both from the federal level and the state level, which can take anywhere from two to six years. Some states have received “State Primacy” status, allowing the state to move ahead in permitting wells. State primacy means that the state rather than the Federal Govt is responsible for permitting, compliance and enforcement of Class VI wells. Getting the CO2 to the sinks will prove challenging, but not due to a lack of storage potential as you can see in the US EPA Geologic Storage Potential map from the US DoE, NATCARB program.

Is CCS currently investable?

Yes! Bloomberg Intelligence has developed a CCUS themed universe which returned 21% on a trailing one-year basis as of June 12, 2024, compared with 18% for the Bloomberg World Industrials Index (WLSTI Index). The top performing exposure category was energy & utilities (24%) and the worst was materials (11%). (06/12/24).6

| Exposure Category | Count | Percent | Region | Count | Percent | MCcap Group | Count | Percent |

|---|---|---|---|---|---|---|---|---|

| Equipment and EPC | 32 | 48 | North America | 25 | 37 | Large | 30 | 45 |

| Energy & Utilities | 20 | 30 | Asia Pacific | 23 | 34 | Mid | 17 | 25 |

| Materials | 15 | 22 | Europe | 19 | 28 | Small | 16 | 24 |

| Ultra Large | 4 | 6 | ||||||

| Total | 67 | 100 | 67 | 100 | 67 | 100 |

While sub-segments of the CCS category include firms across many sectors, including oil and gas majors and industrial gas and chemical companies, there are only a few pure-play public companies.

Capture technology, transport, and storage are additional categories, where incumbent industrials as well as smaller private companies are involved with compression equipment, pipeline engineering and construction companies. Finally, the hydrogen and ammonia integrated companies are also finding profitable projects and are now deploying at scale.

For example, CCS commercial agreements between chemical companies and Oil Industry majors seek to capture up to 2 million tons of CO2 resulting in a “first to market” significant volume of blue ammonia (up to 2 million tons) with virtually all carbon produced from this process captured and sequestered. This will help companies reach their CO2 emissions reduction goal, in some cases of up to 25% by 2030. Estimates of Capital Expenditures up to ~$200M may end up qualifying for tax credits under Section 45Q of the IRA. Two million tons of CO2 tons captured annually will be equal to taking 400 thousand internal combustion vehicles off the road. Companies that supply compressor technologies to the chemical companies will also stand to benefit.

Bioenergy with CCS is also an investable area. For example, Midwestern biorefineries have committed CCS projects through carbon pipeline transport, which will lower GHG emissions through the capture of CO2. CCS is could be a ~$100M EBITDA opportunity annually for biorefineries with several states starting construction in 2025. The net value of the tax credit from Section 45Z of the IRA is likely to be ~$0.30-0.40/gallon range.

Next on the horizon

Uncertainty is rampant in energy markets as well global geo-politics. Where we have more certainty is CAPEX deployed by companies into CCUS. While Net Zero goals by 2050 may seem lofty, the money trail is leading to more advanced CCS as a component of the solution to decarbonizing our economy. Coupled with the other transition topics outlined by Envestnet, capital is catalyzing around decarbonization and sustainable development.

Co-authored by Bruce Kahn with contributions from Elena Chavez and Nicolette DiMaggio of Shelton Capital Management

Note: Shelton Capital Management has or may have a position in the mentioned companies in this report.

To learn more about supporting your clients with sustainable investing solutions, reach out to our team at sustainable@envestnet.com or visit envestnet.com/sustainable.