Rewarded risk factors are recognized as a fundamental component of equity returns. Envestnet | PMC believes that the most robust among the studied risk factors are value, momentum, quality, low volatility, and size. Like all return components, factors are cyclical in nature. Below, we take a look at the performance of these factors in the current market environment.

How factors have fared

Investors hobbled over the finish line battered and bruised by the ups (inflation, interest rates) and downs (valuations of both stocks and bonds) of a tumultuous year. 2022 proved to be the worst year for broad markets since the financial crisis of 2008, as there was little cover from the storm that took both risky and safe assets down in its wake.

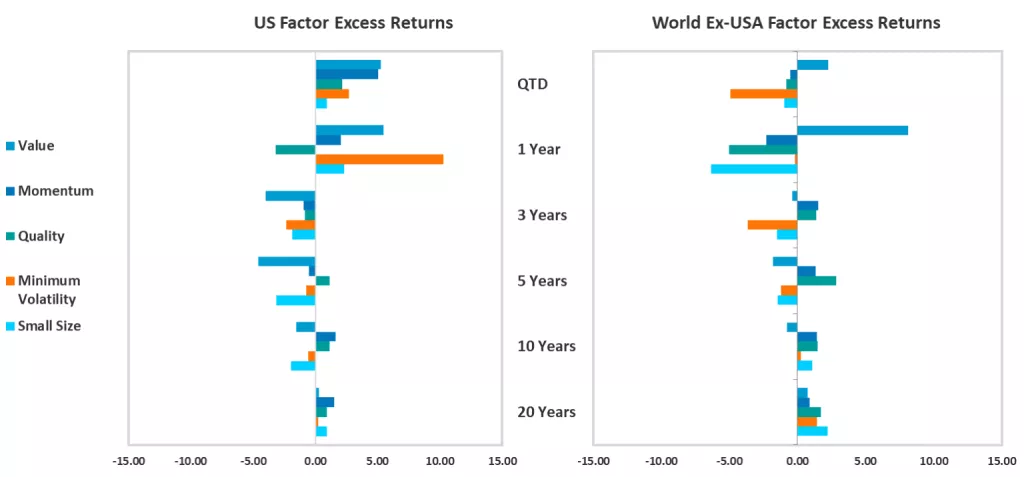

In 2022, some divergence appeared between long-only factor index performance domestically and in markets outside the U.S. While the long-only value factor has been strong and quality was a confounding detractor across the board, others performed differently in the two markets. The size, momentum, and minimum volatility long-only factors were positive in the U.S., while they lagged abroad.

Low volatility was the top-performing of the U.S. indices, shown here for the year, but was virtually flat abroad. The low beta nature of this factor made it a haven for investors seeking safety in less risky assets.

The Graham and Dodd set celebrated some hard-won vindication as they reflected on the year that was, particularly in light of the poor showing for value over the preceding decade or so. The value factor posted the second consecutive year of impressive excess returns, behind only the minimum volatility factor domestically and ahead of all factors abroad. With this year’s win, it has made up considerable ground relative to growth counterparts. For a deeper discussion of the fortunes of the value factor, please refer to this quarter’s Factor Insights piece.

The quality factor in a long-only construct continues to be overshadowed by performance of the market here and abroad. This was particularly true in 2022, given the volatility and magnitude of the valuation adjustment that occurred in the market. The apparent underperformance of the quality factor shown here seems to be a result of market trends, as the long-short calculation of the quality factor has been positive.

Market reaction to higher inflation and interest rates seems to have been to buy value and sell growth. There is some historical correlation between growth and quality, and this selling has been an overall drag for the factor. This dynamic is almost the exact opposite of historical experience in down markets. It is possible that investors are (over)reacting to the bounce in rates from unprecedentedly low levels for an extended period and eliminating from their portfolios anything related to speculative growth, which gets riskier as rates climb. The result is that the market return is dragging down the long-only iteration of the quality index, even as the quality premia itself is positive.

The momentum and small size factors posted relatively modest absolute performance, though small size underperformed more notably abroad.

For a deeper dive on all of these factors, see this quarter’s Factor Insights post.