Investor behavior is complex. To best serve your clients and address the various feelings of fear, excitement, anxiety, and overwhelm that are all too common, understanding investor mindset is key. Envestnet recently engaged with The Center for Generational Kinetics to dig into the mindset and mood of affluent American investors. Our purpose in undertaking this cutting-edge research was to:

- Explore the specific actions, across generations and wealth segments, of affluent Americans when it comes to their financial wellness

- Understand their current mindset about their financial future

We’ve uncovered some hidden behavioral drivers and attitudes, as well as identified impactful data points on both the challenges and opportunities for financial advisors in managing wealth across generational and affluence spectrums. The Great Wealth Transfer has sparked years of discussion on how financial advisors should adapt their practices to cater to the diverse mindsets of investors across generations. But where's the best place for them to begin? Let’s start with research and data. In this post, we’ll focus on exploring differences in investor perceptions and behaviors. We hope you’ll stay tuned for future posts where we share additional findings from our research team to further improve for your practices.

How we define generational groups

For the purposes of our research, we segmented investors into generally accepted generational groups:

While there are certainly pros and cons to generational labels (as noted by institutions like the Pew Research Center), these labels enable us to find and evaluate trends, painting a clearer picture of how large groups of people interact with the world around them. Separating clients into generational segments can often make it easier for advisors to support their clients’ needs, as we’ll see when we dive into the research findings.

How we define wealth segments

For the purposes of our research, we defined the following wealth segments for survey participants:

- Affluent: annual household income or household net worth of >$100K

- High-Earners: annual household income of $200K or more individually, or $300K or more with a spouse/partner in each of the past two years

- High Net Worth: net worth of $1M or more individually or with a spouse or partner

Not surprisingly, there are significant differences between a client with a household net worth of $200K vs. $2M. Now, let's explore how individuals within that wealth segment engage with money according to their generational segment. The differences between a newly affluent younger client and a more established high-net-worth client can be useful for advisors to understand.

Market perception varies by investor segment

Stock market fluctuations, negative economic forecasts, rising interest rates, political uncertainties, and inflation are just a few of the factors that are influencing the attitudes and actions of affluent investors. In the last few years, these challenges and uncertainties have significantly impacted how investors feel about the market.

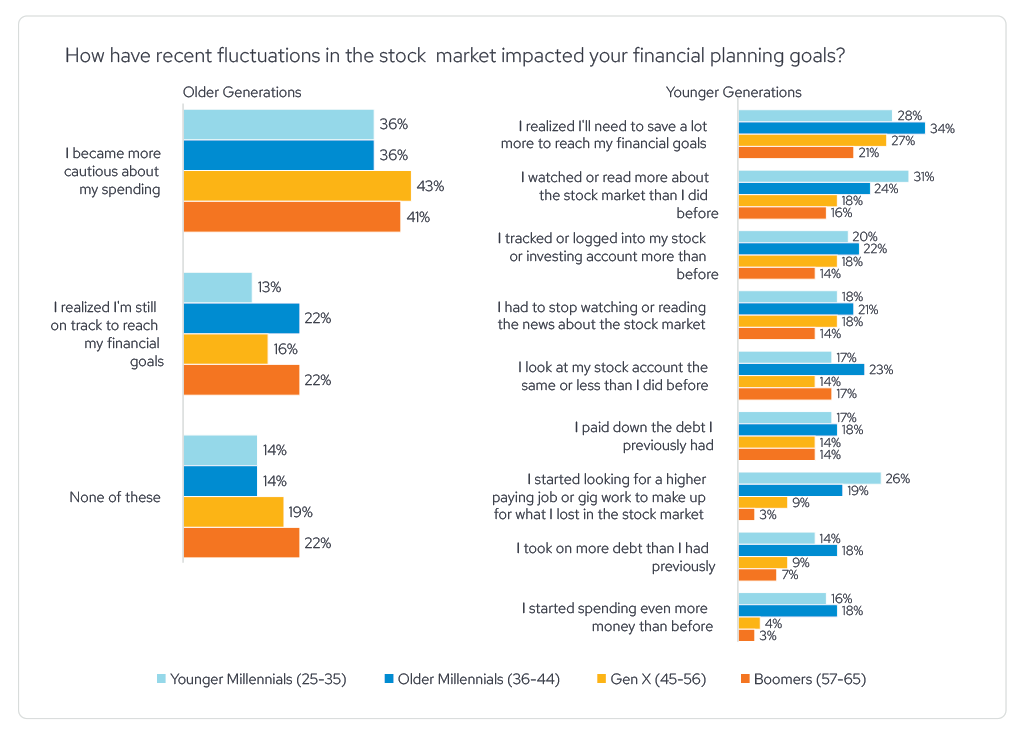

Our research found that older generations are more likely to feel generally cautious about their spending when they see fluctuations in the stock market, whereas younger generations tend to have a stronger reaction. They are more likely to be concerned about their financial security—they might question if they are saving enough, earning enough, and if they are prepared enough for the future.

54% of affluent Americans say recent fluctuations in the market have made them skeptical of investing.

Affluent Americans, across generations have concerns about investing. This skepticism comes from a few different places. Our research found that older generations (64% of Boomers and 57% of Gen X) are more likely to be concerned about market volatility. Is it too risky? Should they adjust their plans? How will the market behave tomorrow? Affluent older generations are also significantly more likely to stay the course regarding their investments, which can be a good thing.

For this group, advisors have an opportunity to help these clients to put the market into perspective. Consider sharing historical market data with your clients that show how diversified or personalized portfolios have performed in times of uncertainty. Help them to see that healthy skepticism is good and your approach (customized to their unique needs) can help them to still meet their goals, even in ‘imperfect’ market conditions.

Younger generations are more concerned about their lack of knowledge about the markets and investing. They aren’t sure how to understand the market fluctuations and if they are prepared or not. Unlike older generations, they perceive their lack of knowledge as their biggest challenge. Interestingly, when faced with market fluctuations, affluent younger generations are also significantly more likely to take action. That action could include diversifying their investing, rebalancing their portfolio, investing less, investing more, losing sleep, pulling money out of the market, switching to another financial advisor, and/or stop investing completely. Their relative comfort with change and interest in learning more can be superpowers when applied correctly.

For this group, advisors have an opportunity to ask questions so they can identify knowledge gaps, as well as areas where the client might be interested in a change. Providing financial education and measured market perspective is a great way to deliver value to younger affluent investors.

Different segments identify different financial challenges

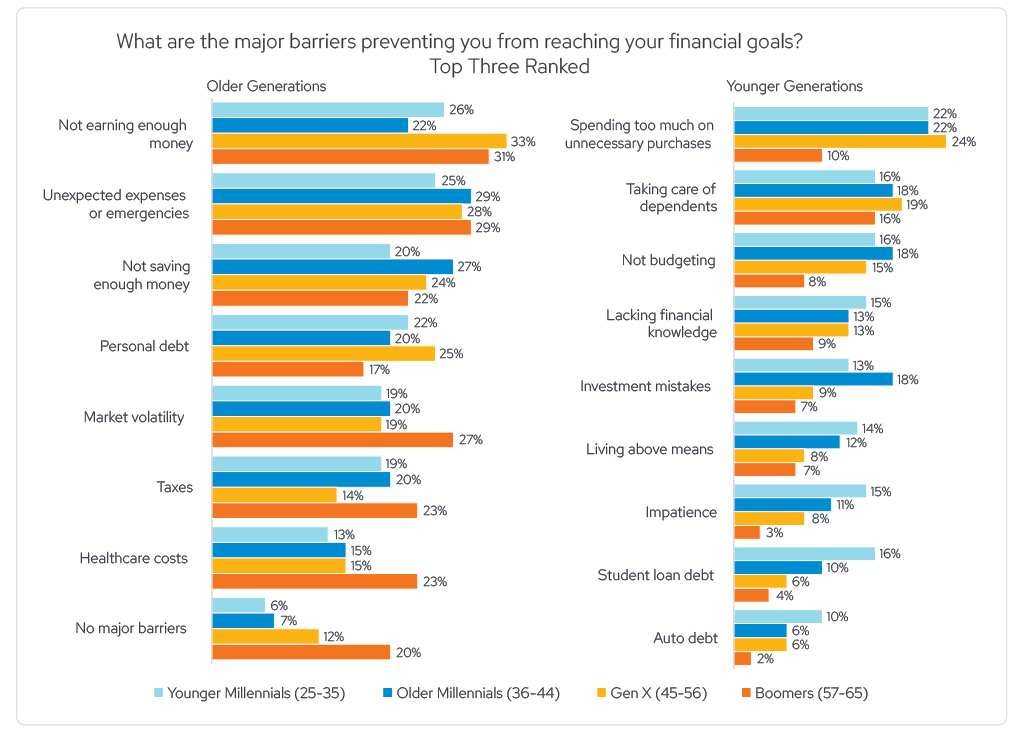

All of the investors we surveyed were asked to rank their top barriers to achieving their financial goals. What is stopping them from living an intelligent financial life? Their responses varied by segment.

For example, Boomers (across wealth segments) identified their top barriers as:

- Not earning enough money

- Unexpected expenses or emergencies

- Market volatility

- Taxes

- Healthcare costs

In contrast, Millennials (across wealth segments) identified their top barriers as:

- Spending too much on unnecessary purchases

- Taking care of dependents

- Not budgeting

- Investment mistakes

- Lacking financial knowledge

When we drilled down into wealth segments, more affluent segments tend to identify taxes as a major concern, just behind market volatility. In fact, both Higher–Earners (28%) and High Net Worth individuals (30%) are significantly more likely than the Affluent individuals (18%) to say that taxes are a major barrier preventing them from reaching their financial goals.

This is very important for advisors to be aware of when engaging in conversations with clients. Learning about the tax impact of different investment strategies, types of accounts, timelines, and tax code changes is important for wealthier clients to understand and feel informed in their investment decisions.

Advisors might consider inviting a tax professional to provide a virtual or in-person informational session for clients and their families. These sessions can be formal or informal and are a great way to show clients that you have the resources they need to think through the tax implications of their investments.

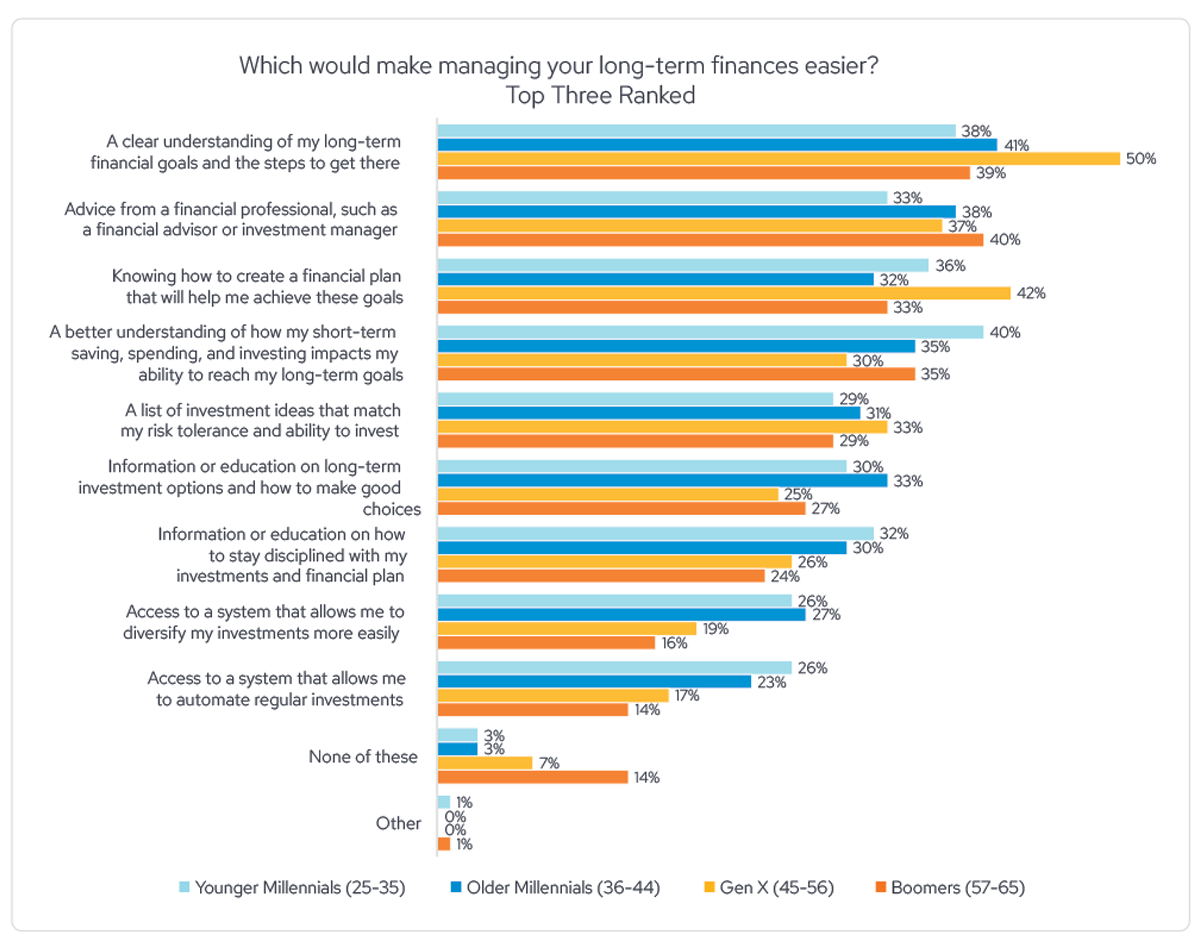

Long- and short-term financial planning varies by generation

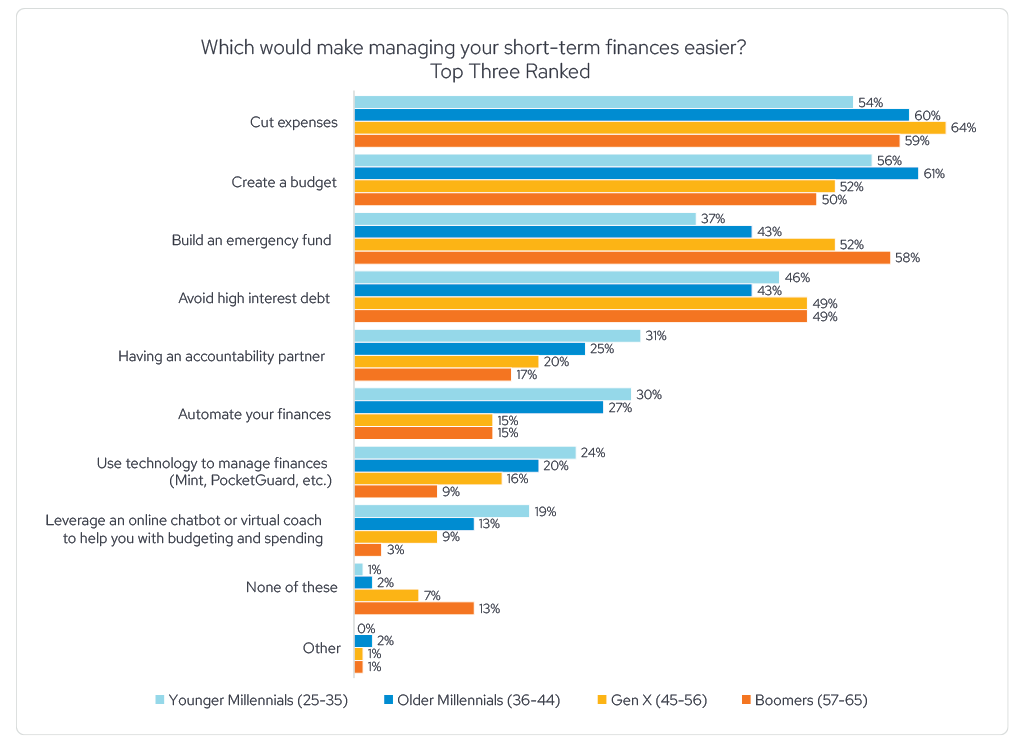

Our research found significant behavioral differences in how different client segments prioritize and manage short- and long-term finances. In the study, younger generations revealed that their top short-term financial considerations included the need to cut expenses and create a budget. They also see strength in automating finances and want an accountability partner.

In comparison, older generations also see the need to cut expenses in the short-term, but in addition, they want to build an emergency fund and avoid high-interest debt. The outlook on life and key priorities clearly varies.

When it comes to long-term financial planning, younger generations are again focused on knowledge gaps. They want to understand how short-term financial decisions connect to their long-term financial goals (a key component of living an intelligent financial life!). They also want information on how to stay disciplined and gain easier access to automation.

In contrast, older generations think a little more linearly about long-term planning. They are focused on the plan itself. They seek a clear understanding of their long-term financial goals and they want a set of clear steps of how to get there.

Advisors use these differences to ensure they provide balanced support to the different client segments they work with. Consider taking note of whether clients are more focused on short-term or long-term goals during your conversations. This insight can provide great clues on where to focus future conversations, while also providing opportunities to connect the two.

Segment your book of business to personalize your approach

When trying to reach financial goals, approaches manifest very differently depending on the age and income of the investor. For advisors, this underscores the importance of individualizing each client’s financial plan. In our research findings, affluent, older generations were significantly more likely to become more cautious about their spending, while affluent, younger generations were significantly more likely to realize that they need to save more, learn more about investing, and start looking for a higher paying job.

Stay tuned for future blog posts on this research! We’ll explore:

- How different client segments feel about the role of the financial advisor and financial advice

- How digital engagement and preferences are evolving

- Trust – how different client segments may feel differently about trusting financial professionals, institutions, and the overall financial services industry

Your clients are not all the same, so approaching their financial needs as if they are could keep you from being as successful as you want to be. We hope advisors can use our research findings to improve how they serve all of the different client segments in their books of business.

Visit https://www.envestnet.com/intelligent-financial-life to learn more about how to guide your clients toward an Intelligent Financial Life using Envestnet's connected ecosystem of tools.